Naked Puts and Leveraged Exchange Traded Funds

Should You Sell Puts on Leveraged ETFs?

I was contacted by a long term reader of the Daily Option Tips and Insights Newsletter who wanted to discuss selling puts on leveraged ETFs.

You can begin receiving the Daily Tips Newsletter yourself by downloading any of the free value investing with options reports on this page.

He'd been selling at the money puts on triple leveraged ETFs 60 days out on one-third of his available capital.

What Are Leveraged ETFs?

An ETF or exchange traded fund is a security that sells on the open market (like a stock) and which is designed to track and replicate the performance of a specific index or sector

Leveraged ETFs take the concept further and are constructed to magnify the performance of the index or sector they track - typically by a factor of two or three.

His reasoning was that if there were a market correction, he would have plenty of cash to sell more puts, and if the market continued moving higher, he was still participating in it.

And since only 33% of capital was leveraged, he felt it was sort of equivalent to what having all his money at work in non-leveraged way would be like.

He also stated that in the event that he was assigned and had to accept delivery of the ETF shares, he would then sell covered calls on those shares as he said I advocated.

(This part isn't exactly accurate, as I address below.)

And then he closed by asking: "Is there is any risk you see with my current strategy? Will be thankful for your input."

What a great topic - and one definitely worth exploring.

I've gone ahead and taken my response to him and adapted it into this full article where I:

- Share some of my thoughts on the strategy as he laid it out

- Identify the potential risks

- Explain why it doesn't quite gel with the approach I teach and advocate

- Still suggest some ideas that might make it safer and more effective for anyone who does want to go this route

Why I Don't Sell Puts on ETFs in General

In theory at least, I like the idea of selling puts (or covered calls) on indexes or ETFs.

But I find there are a couple of important drawbacks when doing so in the real world:

#1 - For the most part, the premium levels are just too low.

Obviously, that's going to vary somewhat depending on what index or sector ETF you're talking about.

But when you're selling options in an overall environment of low implied volatility pricing (which is basically where we are at the time of this writing), then clearly most indexes and ETFs are going to closely reflect that given that they represent wide swathes of the broader market.

#2 - Selling options at the index or sector level removes - for the most part - valuation considerations.

Sure, an entire sector may be beaten down and attractively valued, but an index/ETF that includes both richly valued stocks like TSLA and NFLX along with much more reasonably valued stocks like QCOM or INTC completely removes valuation from the equation.

In a nutshell, I don't sell puts on richly valued growth stocks because the first time they hit a snag, the stock tends to sell off hard.

That repricing of the stock isn't just severe - it can also take a long time to burn off what Mr. Market now views as excessive valuation.

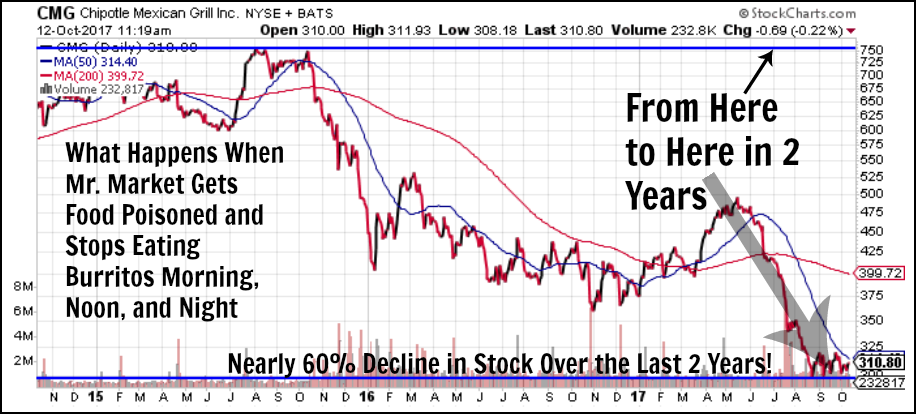

CMG is a perfect example of what happens when Mr. Market falls out of love with a highly valued momentum growth stock that could previously do no wrong:

(click on image for larger view)

VALUATION RESPECT!

I've developed a great deal of respect over the years for the role valuation plays in helping us identify those "Limited Downside Situations."

(Limited Downside Situations = MULTIPLE reasons why a stock is unlikely to trade lower, or lower by much, in the near term.)

Without being able to consider valuation, you're going to be limited to relying solely on technicals when making trade entry and trade management decisions.

I know - there are plenty of pure traders who rely on nothing else.

Just as there are also people who make their living as professional gamblers.

Not saying it can't be done, but it takes commitment, discipline, and a specific type of personality to be successful over the long term.

I know myself well enough to know that's not me - and I don't believe it's most people either.

I want the fix to be in before I ever enter a trade.

I want the structural advantages of working with a customized Strategy where I know that I'll make great returns when I'm right, but can still make decent to good returns even if I'm wrong.

I don't want to be either a genius or a psychic and be right or else I lose money.

WORKAROUNDS THAT MAY NOT WORK

So there are a couple of theoretical workarounds for #1 (low premiums):

>> Set up your trades as credit spreads in order to leverage your capital

>> Or go with those 2-3 x leveraged ETFs.

If you're a reader of Daily Tips newsletter, or if you've spent much time on the Great Option Trading Strategies website, then you probably know I'm not a fan of vertical credit spreads (bull puts, bear calls, and iron condors).

And that's because those spreads are usually used to leverage returns instead of legitimately reducing risk.

You can use them one way or the other, but never both ways at the same time.

I would make a similar argument when it comes to leveraged ETFs - in order to generate attractive returns, you may be taking on a lot more risk than you realize.

Because if you think about it, the leveraged ETF has the same risk-reward profile as the non-leveraged ETF.

But seriously magnified.

What I mean by that is, yes, you may be collecting 3 times as much premium compared to selling a naked put on a non-leveraged ETF.

But on the flip side, you can also get in trouble on the trade 3 times as easily, and you can lose 3 times as much money.

That's the double-edged sword with leveraged ETFs.

You're not just leveraging your potential returns, you're also leveraging your risks.

So you really can't afford to be wrong because the leverage makes it more difficult to repair a short put trade that gets into trouble.

And it's that that makes me nervous selling puts on leveraged securities.

Another thing that would make me nervous is that we've been in an extended period of low volatility with very limited pullbacks.

Even in a healthy bull market, you're going to have 20% pullbacks every once in a while, and with even more frequency, some of those 10%+ pullbacks.

At the time of this writing, It's been a looooong time since we've gotten more than a 3-5% pullback, and we're clearly overdue for something more significant.

That's not to say that the sky is going to fall, of course, but when you're working with an underlying that magnifies market moves by a factor of 3, a 10% pullback becomes a rout, and a 20% pullback may mean that the sky really is falling for you personally.

Holding capital in reserve does help manage the risk.

The subscriber's practice of holding two-thirds of his capital in reserve does help manage his risk.

My only concern is that it may not be enough if/when we get a significant correction.

Again, with these kinds of leveraged securities, any pullback is going to be magnified by a factor of three.

Technical-Based Trading

So if you are going to sell puts on leveraged ETFs, I think it really become paramount that you be comfortable with and adept at trading based on technicals.You really need to be able identify the prevailing trend, where support and resistance are, when the underlying is technically overbought or oversold - and then incorporate that into your setups and trade management decisions.

If that's the only tool you have, you really need to get good using it.

Repair? Or Run?

And if the trade moves against you, while the additional capital on the sidelines may help to get you out of minor scrapes, it's probably not going to be enough to protect you against moderate (or worse) pullbacks.

So your best bet may be to cut your losses rather than trying to repair them.

The reason why I'm so comfortable sticking with my "bad" trades and repairing them is because I know the downside is almost always contained and limited.

Booking a loss on a short put trade as we employ the strategy is almost always a mistake because it's almost always unnecessary.

See:

Why Stick with a Losing Trade?

And even if I blow it and I'm totally wrong and the underlying stock still takes a big tumble, the 4 Stage Short Put Trade Repair Formula I developed is proven and effective enough to be able to repair even the hairiest of trades.

The underlying principles of the Trade Repair Formula can still be used when selling puts on leveraged ETFs, of course.

But I just think in any market that's not a strong bull market, you're going to find yourself in quite a lot of those "hairy" trades.

And that's especially true if you're just indiscriminately selling at the money puts with no consideration of the technicals.

What About Assignment and Then Writing Covered Calls?

The subscriber also mentioned the idea of allowing assignment on his in the money (ITM) short put positions and then selling covered calls against the assigned shares.

That's not actually our repair strategy inside The Leveraged Investing Club.

Or rather, we only allow assignment and begin selling covered calls VERY reluctantly, and even then, only on a portion of our larger position.

It's basically our last line of defense, not our first.

It's also a testament to the 4 Stage Short Put Trade Repair Formula that it's extremely rare that we ever find ourselves selling covered calls because a naked put trade went against us.

The biggest risk to selling covered calls on shares assigned from short put trades that went against us is the risk of being whipsawed at some point.

If pullbacks are short and shallow, as they have been for quite a while now, you don't have this problem.

But the more the underlying ETF sells off so that there's a big difference between the strikes where you're selling covered calls vs. the strikes where you were assigned on the short put side of the ledger, the greater the risk of being whipsawed if/when that ETF makes a move back to the upside.

It can easily become a case of buying high (assignment on in the money short puts) and selling low (assignment or being underwater on in the money short calls).

A deep in the money short put position that you hoped to recoup/repair by allowing assignment and then selling covered calls is itself at risk of trading deep in the money and building up unrealized losses (which you may or may not be able to avoid realizing) in the other direction.

Check out this 2-1/2 year chart on TQQQ:

{kind=link}

(click on image for larger view)

Twice - in the summer of 2015 and at the beginning of 2016 - TQQQ fell from the low to mid-$60s all the way down to the mid-$30s in pretty short order.

Both times the market recovered, but in volatile, W-like fashion.

W as in Whipsaw.

You easily could've been in a situation where you sold puts @ the $60 strike, the trade goes against you massively, then you sell covered calls @ $40 and the same thing happens to you again in the other direction.

And it happens to you more than once because it's a W-shaped recovery rather than a V-shaped one.

And both of those sell offs represented corrections in the broader market of less than 20%.

Keeping a lot of cash in reserve can definitely help you navigate all that.

But my concern is that even as much the reader who contacted me was holding back, it still might not be enough in the event of a more serious correction, or in the event that real volatility returns to the market (which it always does at some point, of course).

So again, I think if you trade this strategy, you may need to do so more as a traditional trader would.

That means trading based solely on technicals (or even probability analysis if you prefer) and then cutting your losers short rather than trying to repair them.

Because there are very real scenarios that make it difficult if not impossible to repair these kinds of trades.

And staying with a trade that you can't repair is only going to magnify your losses.

The downside to trading solely on technicals is that it's a lot harder than it looks.

Technical analysis tells you what HAS BEEN happening, not necessarily what WILL happen.

Or rather, it tells the past and the present which we can use to make an educated guess about the future - but it never tells the future on its own.

It's an important tool, and one I use myself, but only having one tool on your tool belt really limits your flexibility and forces you into needing to be right on what the underlying is or isn't going to do.

Stacking the Deck

That's not a position I want to be in at all.

The more factors I can line up on my side ahead of time (such as valuation), the more I limit the downside in a trade, and the easier it's going to be to repair it anything goes wrong.

In other words, the consequences of being wrong are much less severe.

That's why I rarely ever book a loss, and why I also rarely ever have to resort to selling covered calls on assigned shares.

I use the analogy of a team sport where you have both offensive players and defensive players.

With the Sleep at Night High Yield Option Income Strategy, our trades have a healthy mix of both.

If your trades only make money when you're right (and lose - a lot of - money when you're wrong), you're playing a sport without a defense.

And it's not hard to predict what's going to happen to your team over the long term.

Tweet

Follow @LeveragedInvest

![]()

>> The Complete Guide to Selling Puts (Best Put Selling Resource on the Web)

>> Constructing Multiple Lines of Defense Into Your Put Selling Trades (How to Safely Sell Options for High Yield Income in Any Market Environment)

Option Trading and Duration Series

Part 1 >> Best Durations When Buying or Selling Options (Updated Article)

Part 2 >> The Sweet Spot Expiration Date When Selling Options

Part 3 >> Pros and Cons of Selling Weekly Options

>> Comprehensive Guide to Selling Puts on Margin

Selling Puts and Earnings Series

>> Why Bear Markets Don't Matter When You Own a Great Business (Updated Article)

Part 1 >> Selling Puts Into Earnings

Part 2 >> How to Use Earnings to Manage and Repair a Short Put Trade

Part 3 >> Selling Puts and the Earnings Calendar (Weird but Important Tip)

Mastering the Psychology of the Stock Market Series

Part 1 >> Myth of Efficient Market Hypothesis

Part 2 >> Myth of Smart Money

Part 3 >> Psychology of Secular Bull and Bear Markets

Part 4 >> How to Know When a Stock Bubble is About to Pop