Less Risk Selling Puts

Or How I Used a Put Selling Campaign to Lock in 15.51% Annualized Returns Over 172 Days on a High Quality But Struggling Stock While Significantly Reducing My Risks

Got a cool example of something I want to illustrate for you today on the topic of how trading options can actually reduce and even eliminate risk - while still helping you make terrific returns.

Bear with me - I want to talk you through the concept and then I'll show you a real world example to illustrate.

The Peril and Promise of Trading Options

Option trading often gets a bad rap because of the leverage factor and how easy it is to increase your risks in pursuit of big speculative paydays.

(And, I would argue, traders often assume, or rationalize, a lot more risk than what they realize.)

In fact, options first came into existence as a way to help investors MANAGE risk, not play the ponies or shoot craps.

Myself, I see options as an amplifier - they take any market approach and magnify it.

Sure, a lot of the time that may mean speculation on steroids, but it doesn't have to be that way.

Option trading can also be designed in a way that emulates - and improves - a proven, Warren Buffet style value investing approach.

That's why I love so much a strategy as simple and straightforward as selling puts - because it can be calibrated to be a serious synthetic value investing instrument.

(Most of the time it isn't, of course, as generic, two-dimensional trading approaches dominate the stock market - not being an elitist, just being honest.)

There's an old value investing principle that says the purchase price of a stock is far more important than the selling price.

That's because the lower your cost basis, the greater the impact each dollar of share price appreciation (or dividend income, for that matter) has on your returns.

And not only can selling puts on your favorite stocks also capitalize on this principle - it's actually a far easier and a much quicker process than traditional value investing stock ownership.

Why?

Less Risk Selling Puts - The Power of a Put Selling Options Campaign

When you purchase shares, your cost basis on those shares is exactly what you pay - and it remains a static figure until or unless you add more shares.

If you add shares to your position, you then combine and average your purchases to determine your new static cost basis.

But get this - not only will your cost basis be lower when you sell puts vs. buying the stock on the open market, but if you play your cards right, that cost basis can keep going down.

Again and again and again.

Cost basis on shares you don't even own?

What the heck am I even talking about?

You can also think of it in terms of breakeven.

After all, that's essentially what the cost basis on a long stock position tells you anyway - the share price boundary between unrealized gains and unrealized losses.

Cost Basis - Long Stock vs. Short Puts

We'll exclude commissions to keep everything simple, but if you pay $30/share acquiring a stock, your cost basis - and breakeven - is that same $30/share.

If, however, you sell a $30 put on the stock and collect $0.50/contract in premium, your breakeven - or cost basis if theoretically assigned - is $29.50/share.

Big deal, right?

It's a huge deal - because it doesn't have to be a one-time event.

Because what happens when you're able to keep a trade going?

When you're able to continually roll it out for repeated net credits?

(i.e. you collect more in new premium for selling a new put farther out in time than what it costs you to close out the old or expiring one.)

As you continue bringing in more and more net premium, your breakeven and cost basis on the position plummets.

And this is important - and a big deal - even if you never have any intention of owning the shares.

The cost basis/breakeven on a short put position has two functions:

>> It lets you know how much of a buffer you have for a stock to fall before you're technically underwater on a trade

(Remember - stock only investors with their one-time static cost basis have no buffer without the underlying stock moving higher first.)

>> You can also use it to calculate your option income returns on the position

Again, you can make terrific returns selling puts without ever owning - or intending to own - the underlying shares.

It's almost like a synthetic stock ownership position but one where you get to keep reducing the amount you paid for your position.

(Your total accumulated net premium on a position divided by your cash-secured capital requirements gives you your total ROI - and from there it's easy to annualize to give you a frame of reference - here's an article and how to calculate your annualized returns - and why it's one of my favorite metrics.)

So when you're in campaign mode vs. single trade mode, the longer you stay in a trade, you gain a double benefit:

>> More Gains

>> Less Risk

Let's look at a real world example to illustrate the power of this approach . . .

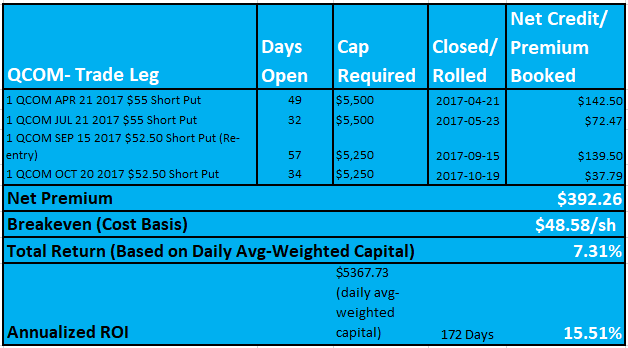

The QCOM Naked Put Campaign

This is a perfect example of less risk selling puts through an orchestrated put writing campaign.

Throughout 2017 I wrote puts on QCOM when the stock traded in the low to mid $50s - a level that I found attractive from a value investing perspective in terms of valuation and dividend yield.

(I also used basic technical analysis to help me with timing my entries and adjustments - all stuff covered in the periodically offered Sleep at Night High Yield Option Income Course.)

All told, there were four separate legs of the trade, and taken in their entirety, the trade produced 15.51% annualized returns on a daily average of $5367.73 of cash-secured capital over 172 days:

Now, there are some important points here:

#1 I ended up flubbing my final exit of the campaign - I closed the position the day before the October 20 2017 expiration when the position was trading a bit in the money (i.e. below the $52.50 strike price of my short put).

But QCOM rebounded the next day so that the $52.50 short put would've expired worthless after all

Had I done nothing, my final returns would've been 17.14% annualized over 173 days vs. the 15.51% annualized over 172 days that walked away with.

#2 I decided to end the campaign rather than roll it once again because at that point, there was an earnings release in a couple of weeks and I preferred to avoid that potential risk

Again, in hindsight, the better move would've been to roll the position for a nice, juicy net credit (because of the elevated premium associated with the upcoming earnings release plus the fact that the stock was trading near the money as well).

While the stock did initially drift back down toward $50, at the beginning of November, AVGO made a bid to buy QCOM for a whopping $100 billion and the stock shot up into the mid to upper $60s.

#3 There are no crystal balls! It's much more important, in my view, to have the clarity to make informed choices about what's best for a trade rather than kicking yourself for not being psychic.

So even though there were things I could've done differently in hindsight to improve the results, I feel I made sensible and conservative choices - and I'm thrilled with the returns the campaign produced.

Big Benefits of Selling Puts in Campaign Mode

But let's get back to the original point of this article - the benefits and power of an orchestrated put selling campaign on a stock.

As you can see in the Trade Performance Table above, the campaign produced excellent results @ 7.31% total returns over 172 days, or 15.51% on an annualized basis.

Keep in mind that the stock was generally flat to down during the time period in question, so 15.51% annualized clearly smoked whatever flat to negative returns stock-only investors generated during the same time period.

(At the strike prices I was dealing with, the stock did have a 4%+ dividend yield, so at least stock-only investors were getting paid something.)

Yes, we know that option trading can give us above average returns.

But if you have to assume above average risks in order to get those returns, it's not going to be worth it.

As I like to say, high risk doesn't mean that you've got a chance at doing better than everyone else - it means that it's only a matter of time before you blow a gaping hole in your portfolio.

So despite locking in a 15.51% annualized ROI over an extended period of time on a struggling stock, a QCOM campaign is only smart providing I didn't jack up my risk in the process.

But here's the deal - not only did I not increase my risk with the way I structured the campaign - I significantly DECREASED it.

Check out the Trade Performance Table again:

The campaign accumulated $392.26 of total net premium when the dust settled.

In other words, after I was completely out of the position, I had $392.26 more than I started with.

When you deduct that accumulated net premium from the $52.50 strike price (and multiply it by 100 shares), you get an effective breakeven (or cost basis) of $48.58/share.

Keep in mind that I originally started the campaign at the $55 strike when the stock was trading in the mid-$50s.

That's where a comparable stock-only investor would've initiated his or her position - and the moment the shares dipped below that purchase price, those shares would then be underwater.

In contrast, in a worst case scenario, by the time I exited my value investing with options version of the investment, QCOM would've had to trade below $48.58 before I started feeling any pain whatsoever.

Of course, because my campaign had so many structural advantages built into it, even if the shares had traded down to those levels, I still had an entire unopened bag of tricks at my disposal to repair the position.

(By - you guessed it - continuing to work the cost basis/breakeven lower and lower and lower some more).

By the time my position was underwater again, the comparable stock-only investor who entered a position at the same time I began my campaign would've been DOWN more than 12%.

THAT'S the power of a put selling campaign.

When you apply a campaign to a structurally advantaged strategy and when you approach that campaign from a value investing mindset, you don't just set yourself up to make great returns.

You also reduce - and even eliminate - risk in the process.

No joke - better returns and with less risk.

(And that's why the customized put selling strategy I advocate and teach is called the Sleep at Night Strategy.)

HOME : Naked Puts : Less Risk Selling Puts

![]()

>> The Complete Guide to Selling Puts (Best Put Selling Resource on the Web)

>> Constructing Multiple Lines of Defense Into Your Put Selling Trades (How to Safely Sell Options for High Yield Income in Any Market Environment)

Option Trading and Duration Series

Part 1 >> Best Durations When Buying or Selling Options (Updated Article)

Part 2 >> The Sweet Spot Expiration Date When Selling Options

Part 3 >> Pros and Cons of Selling Weekly Options

>> Comprehensive Guide to Selling Puts on Margin

Selling Puts and Earnings Series

>> Why Bear Markets Don't Matter When You Own a Great Business (Updated Article)

Part 1 >> Selling Puts Into Earnings

Part 2 >> How to Use Earnings to Manage and Repair a Short Put Trade

Part 3 >> Selling Puts and the Earnings Calendar (Weird but Important Tip)

Mastering the Psychology of the Stock Market Series

Part 1 >> Myth of Efficient Market Hypothesis

Part 2 >> Myth of Smart Money

Part 3 >> Psychology of Secular Bull and Bear Markets

Part 4 >> How to Know When a Stock Bubble is About to Pop